Notes on Revenue-Based Financing

Notes on Revenue-Based Financing

European Straits | Work in Progress

Hi, it’s Nicolas from The Family. Here are some further thoughts on what I’ve decided to call the ‘diffraction’ of venture capital, specifically revenue-based financing.

Alex Danco, who is now with Shopify but was long the in-house blogger at Chamath Palihapitiya’s Social Capital, wrote a great piece earlier this year about debt slowly replacing equity as the preferred option for funding tech companies. This was one of my major inspirations in writing The Diffraction of Venture Capital. But I wasn’t the only one for whom Alex’s piece triggered a chain of thoughts. Indeed, a whole discussion is still going on, notably on VC-oriented Twitter and blogs, about one particular wave in the current diffraction: the rise of revenue-based financing. Can you turn a tech company’s revenue into collateral to issue securities and raise debt from investors on the fixed-income market?

1/ The idea of revenue-based financing is not exactly new. I often use a quote from The Partnership, Charles D. Ellis’s wonderful book about the history of Goldman Sachs (I used it a lot when writing my 11 Notes on Goldman Sachs), to explain what financial innovation is about. It tells us about the moment when Henry Goldman, the son of the bank’s founder Marcus Goldman, convinced investors on the bond market to lend money to a retailer with their future revenue as a collateral.

When I’m in a hurry, I hastily explain that Goldman more or less invented the technique of discounting cash flows, which is obviously not really true. Nevertheless, his relentlessness contributed to shifting market practice and convincing generations of investors that they can lend money to a company based on future earnings rather than fixed assets. Here’s the quote again:

The public securities markets, both debt and equity, had always been carefully based on the balance sheets and the capital assets of the corporations being financed — which is why railroads were such important clients. To expand, United Cigar needed long-term capital. Its business economics were like a “mercantile” or trading organization’s — good earnings, but little in capital assets. In discussions with United’s half dozen shareholders, Henry Goldman showed his creativity in finance: he developed the pathbreaking concept that mercantile companies, such as wholesalers and retailers — having meager assets to serve as collateral for mortgage loans, the traditional foundation for any public financing of corporations — deserved and could obtain a market value for their business franchise with consumers: their earning power.

2/ Can we reenact Henry Goldman’s stroke of genius, this time for the new giants of the day—not mass retailers, but tech companies? This is a question I’ve been asking myself a lot, without making much progress. But the concept of revenue-based financing has been discussed so much recently, including within the financial services industry, that I’m now sure the answer is yes, and practices will soon start to shift. Here are a few examples:

In my piece on The Diffraction of Venture Capital, I mentioned the case of OATV’s Indie.vc. Here you will find more details about the terms they offer in v3 of the program: “The benefit to founders is an opportunity to own and control more, not less, of their company and destiny over time. The benefit to investors is to be able to realize a return through a revenue share that gets treated as gains instead of income. All without the pressure to exit.”

There’s also this article in TechCrunch about how Startup investors should consider revenue share when equity is a bad fit: “A revenue-share deal typically involves a capital investment that is later repaid from a share in the revenue of a growing business. It has historically been used to invest in businesses with potentially predictable cash flow and high profit margins, from Hollywood movies to high-margin service businesses.”

David Teten, an investor and leading thinker about innovation in venture capital, wrote about Revenue-based investing: A new option for founders who care about control: “A new wave of Revenue-Based Investors are emerging who are using creative investing structures with some of the upside of traditional VC, but some of the downside protection of debt. I believe that Revenue-Based Investing (“RBI”) VCs are on the forefront of what will become a major segment of the venture ecosystem. Though RBI will displace some traditional equity VC, its much bigger impact will be to expand the pool of capital available for early-stage entrepreneurs.”

Sifted has recently covered the topic in It's finally the moment for revenue-based startup financing: “Unlike equity financing, revenue-based financing is a fixed sum that’s repaid over time based on incoming revenue. Founders receive money from an investor to spend on marketing or inventory, and with every sale they make, they repay a percentage of that loan. A company might receive €100k, and would then repay 5-20% of every future sale back to the investor until the amount is repaid in full — with a fixed fee on top. Typically there are no equities, personal guarantees or hidden fees involved.”

Conor Durkin was prompted by Alex’s piece to reflect on how this reasoning applies to the Software-as-a-Service industry. Have a look at Some thoughts on SaaS ABS: “At a high level, the point is pretty simple – most SaaS businesses have, for a given cohort of customers, a pretty predictable and regularly recurring cashflow stream. That, fundamentally, looks a lot like a fixed income instrument like a mortgage or a student loan or any other asset which spits off similar-ish amounts of cash every month and has some nonzero chance of getting cut off at any point in time (like a mortgage borrower defaulting, or a SaaS customer cancelling a subscription).”

Finally, here’s John Luttig of Founders Fund also echoing Alex Danco: “As Alex Danco highlighted in his recent article Debt is Coming, it is clear that recurring revenue securitization – the notion of selling your future ARR bookings at a discount – is the future. The biggest barrier to adoption is cultural: the stigma that “venture debt is like a delicious sandwich that only costs ten cents, but occasionally explodes in your face” is deeply tied to the predatory reputation of old-school venture debt lenders. Companies like Pipe and Clearbanc are already starting to destigmatize securitization, and it will only become more culturally normalized in the coming years.”

3/ I think the best starting point for reflecting on revenue-based financing is to come back to the definition of a tech company. I’m not sure there’s one that’s won out yet, so let me propose my own (based on how I define the Entrepreneurial Age):

A tech company is one that harnesses more power outside than inside its organization.

Let me also quote one of my old essays, Capitalists Beat Merchants Every Time:

A key feature of tech companies: they accomplish a lot without immobilizing as many assets or employing that many people. This explains the high rate of return on equity for those who make it to a successful exit (Instagram) or to perennial domination (Facebook).

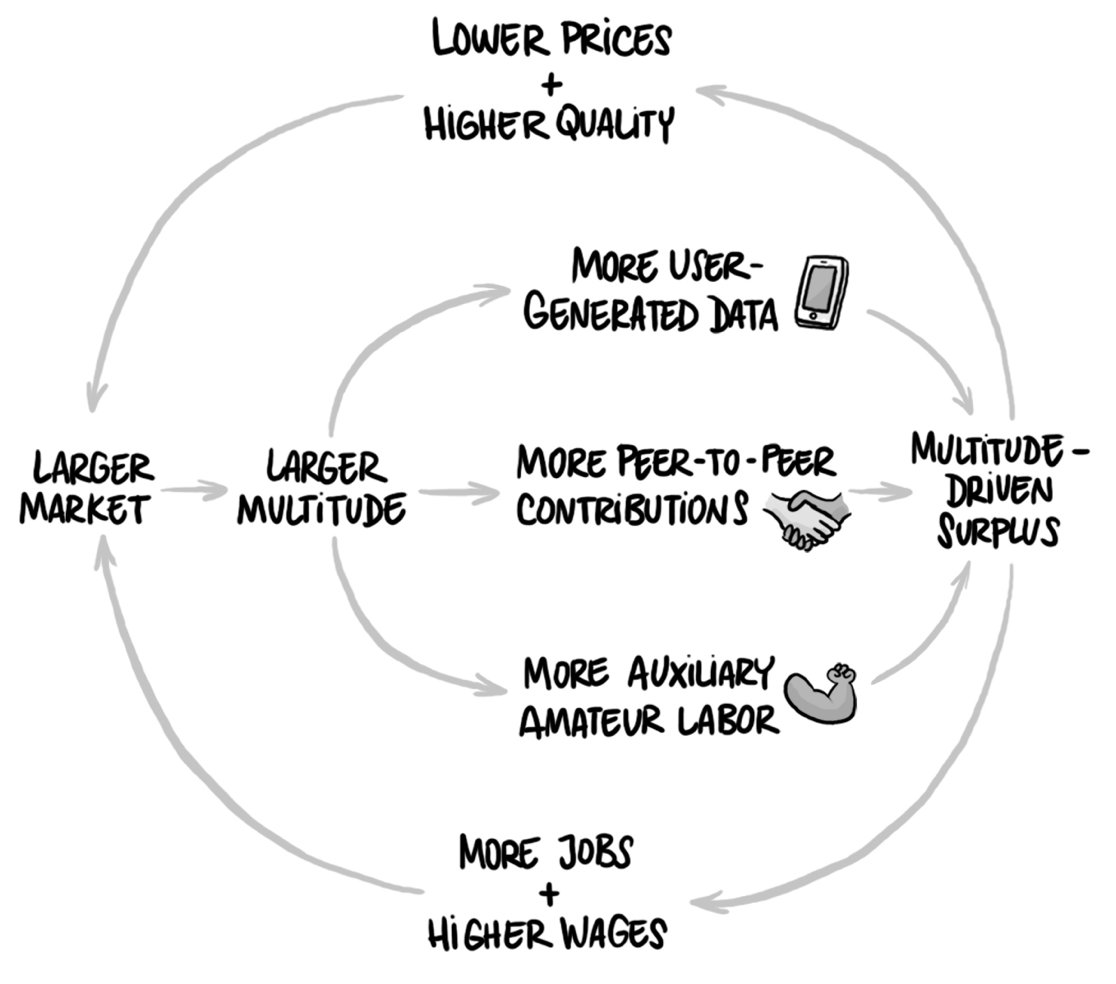

What I’m talking about here is the network of users (what I call the “multitude”), and the fact that they’re more than mere customers: they not only pay money (sometimes), they also contribute to creating value through data collection, peer-to-peer interactions, and occasionally lending a cheap hand in exchange for money. About that, here’s an illustration from my book Hedge:

4/ How does it apply to reasoning on revenue-based financing? At first sight, most tech companies have exactly the same problem as those retailers for whom Henry Goldman had to raise money over a century ago: they have future revenues but no tangible assets that could serve as collateral. Given that, there’s room for bringing in revenue-based financing just as Goldman did.

But I think that we need to go one step further when applying this reasoning to tech companies. We need to realize the nature of a user base (which is different from a customer base), the fact that it directly contributes to value creation, and as such that it has the same nature as an asset. Let me quote Capitalists Beat Merchants Every Time again:

If bonding with the multitude [of users] equals additional capital in the future, it can be accounted for with a net present value—like any other asset (even though it cannot be accounted for on the balance sheet). One challenge is to calculate the value of a company’s alliance with the multitude in the future: this requires projecting what users bring to the table as well as the various technology-driven positive feedback loops (among them network effects—here’s the microeconomics). Another challenge is to infer the net present value of that alliance by applying a discount rate (here comes corporate finance).

5/ At this point, you can see why SaaS is the perfect solution to turn the distinctive nature of tech companies into revenue-based financing. For any good SaaS product, users are very much part of the value chain. But the design of the product as well as the various feedback loops constitute a moat that enables SaaS entrepreneurs (and their investors) to more effectively predict growth and revenue in the future, therefore turning the system into the base for raising capital from investors.

Here’s John Luttig again:

A large portion of the collective effort of VCs is focused on late-stage software financings. This certainly will not go away, but companies with predictable metrics will have access to alternative financing options like debt and securitization products.

6/ Another question: Can the revenue-based financing techniques pioneered in the SaaS world be expanded into financing tech companies that don’t belong to this narrow category? This is where it gets tricky. To reflect on that, let me quote my Principles for Capital Allocation (Round 1):

We’ve long entered a world where all businesses are hybrid—part software, part non-software. The whole question is the balance between the two. We can see it as a sliding scale, from Category 1 (no software) to Category 5 (pure software).

Knowing where a business stands on that scale is the most important thing anyone (executives, investors) should have in mind if they want to succeed in the Entrepreneurial Age.

From Category 4 upward, the network effects derived from software (demand-side economies of scale) dramatically outweigh the supply-side economies of scale (large volumes, lower unit costs). Unit economics depend on the category to which the business belongs. It then commands a specific approach to capital allocation to make the most of the company’s distinctive value chain. Again, software is all scalability (you can grow very quickly as long as there is room for it); at the other extremity, non-software is defensibility (it's difficult for a new entrant to compete with you).

7/ The truth is, we should learn to differentiate funding a tech company depending on its stage and the different parts of its value chain. Let’s start with the different stages:

At pre-seed and seed, the criticality of risk is clearly different as the company progresses. At the seed stage, the probability of failure is high but the potential impact of the failure is low. This typically lends itself to equity financing from investors (angel investors, seed funds) with a portfolio of participations broad enough so as to offset the many losses with a few good wins.

At the Series A stage (when the company has passed product-market fit), the risk of failure goes down and the impact is still small, so overall the risk is not that critical. However, the absence of solid data makes it difficult to assess that risk and to reliability predict growth. It’s still too early to extrapolate and determine how much the company will make in the future. So until the company gets a firmer foothold in the market, we’re still in the realm of equity financing.

Series B is when things become much clearer, but also when the competition heats up, which means that the risk of failure becomes more critical (lower probability, but much higher impact), yet on the other hand there’s now the “clearer understanding of their growth levers”mentioned by John Luttig. This, I think, is a stage where companies should start to diversify their financing, with the residual risk being borne by equity investors while funding predictable growth can be covered by securities backed by some fraction of the revenue being generated.

This still feels a bit blurry for me, but I’ll keep iterating on the extent to which each stage potentially lends itself to revenue-based financing rather than traditional venture capital.

8/ The ability to use revenue financing also depends on the category (on the 1-to-5 scale) to which the company belongs. This is a spectrum where:

Category 1 (“essentially tangible activities with a little bit of software”) comes with straightforward collateral for debt financing, but not much room for scalability.

Category 5 (“a business that relies so much on software that it doesn’t have tangible assets on its balance sheet”), on the other hand, is highly scalable but needs to get the flywheel going to be able to raise from providers of revenue-based capital.

This makes me think we should reason not with two categories (equity financing and debt financing), but rather with several categories depending on various collaterals, and push the various buttons in different ways depending on the stage and the business the company is in.

9/ Ideally, one would have to separate the different parts of the company’s value chain and fund them differently depending on the underlying economics. However there are three limits to doing that:

One is that capitalism’s best practices tend to lead companies to outsource what doesn’t fit into their core business’s economics. Hence tech startups rely on AWS rather than having to own or rent their own physical servers. You might be able to raise debt with the servers as collateral, but it’s so much simpler to pay the equivalent of interest on the debt to AWS so that it takes care of the entire server dimension of the business. The same happened with WeWork: they were signing leases rather than owning real estate even though property could have been used as collateral to borrow more money—and it was good practice!

Whatever parts of the value chain are still owned and operated by the company itself, it’s usually difficult to separate them in different financial layers. It’s good practice, from a corporate strategy perspective, to make every component of a company’s value chain “fit” together (Michael Porter’s word) so as to make them impossible to separate. In fact, only very large companies offload entire parts of their value chain because they don’t fit into the specific economics of the core business and call for other approaches to financing: see the examples of McDonald’s (every franchise, really) and the interesting corporate case that is Coca-Cola.

Finally, the last obstacle to diversifying financing as a company grows is the fact that equity investors have made big bets early on (typically, these are venture capitalists) and they don’t want more senior debt investors coming to the table later so as to deprive them of their precious upside. This is why raising large debt rounds, as in Airbnb’s case recently, can only work for very large companies, those able to negotiate ad hoc deals and where early-stage investors have already secured a significant upside thanks to secondary deals and a favorable preference stack.

As an illustration for this whole part of the discussion, you should really listen to this podcast in which Benchmark Capital’s Bill Gurley, then an investment banker, Mary Meeker, Michael Mauboussin, and Kara Swisher tell the story of Amazon issuing bonds rather than raising more venture capital to fund its growth in 1997-1998 (starting at 13:00). It was all done thanks to the brilliant Jay Covey, then Amazon’s CFO, and without Jeff Bezos being allowed in the room—because, quite simply, Covey and the potential bondholders needed to have a practical conversation about numbers, assets and revenues over the short term, not the long-term vision of the inspirational empire builder that Bezos already was.

10/ In conclusion, I’m still wondering why tech founders still have to promise so much upside to venture capitalists in a world where capital has become so abundant and cheap. Several hypotheses could explain it:

We’re still waiting for a big wave of financial innovation up the stream, whereby brilliant financiers such as Henry Goldman will convince institutional investors to allocate capital to debt funds that will then be deployed across the whole tech sector in the form of revenue-based financing. (Otherwise they could act on a mandate from the company and raise money for one client only.) This (institutional resistance to the rise of a new asset class) is all well explained in Conor Durkin’s piece quoted above.

We still don’t have a clue of what happens if a fast-growing tech company defaults on its debt. Maybe it will be because the founding team is not delivering a good-enough product, in which case you can replace the team (but that’s not a banker’s job) or you can sell the company to a bigger acquirer that will upgrade the product and make the most of the existing user base. Or maybe it’ll be because a better competitor has entered the market (like Slack challenging Hipchat back in the day or Microsoft Teams challenging Slack right now)—and that, despite the progress in growth accounting, remains difficult to predict.

The last hypothesis is that the abundant capital is so concentrated in the hands of just a few players that they’re terrified of losing it (after all, it’s so much money) and are reluctant to agree to experiments like revenue-based financing when they can make so much money in more familiar segments of the market. This was voiced by Matt Stoller in his interesting How Monopolies Broke the Federal Reserve, and it would call for determined action from governments: only new regulations, safeguards, hedging mechanisms, and institutions can lead capital away from traditional allocation and toward something such as revenue-based financing.

To be continued! What are your views on revenue-based financing? Have you stumbled across promising cases, or, on the contrary, experiments that turned out to be resounding failures? I look forward to hearing from you as I’m convinced this discussion is critical for Europe and the tech world in general.

From Paris, France 🇫🇷

Nicolas